"Chris Martinez: Preparing Your Agency for Sale (EBITDA Multiples, the Three Must-Dos, Earn-Outs)"

Chris Martinez of Bloom Partners condenses his exit playbook: the real take-home math behind a sale, the full sell-side process, and the three areas buyers scrutinize (financials, team, customer acquisition and retention).

On this page

Chris Martinez, founder and partner of Bloom Partners and now President (moving to CEO) of BPO Solutions Group, gave a condensed version of his usual six-hour "3 Must-Dos to Prepare Your Agency for Sale" talk. His core message is that revenue is vanity and profit is sanity, so all that matters at exit is what you keep. He walks through the real take-home math of a sale, the step-by-step sell-side process, and the three things buyers actually scrutinize.

Main takeaways

-

A CEO's one job is to increase the enterprise value of the company year over year. Martinez frames everything else (team, financials, acquisition and retention) as serving that single metric, and says to hold yourself to the same standard you would hold a CEO you hired.

-

The headline sale number is not what you keep. Stress-test it: cut the enterprise value in half (you typically get half in cash at close and half in an earn-out the buyers may never pay out), reduce by about 40% for worst-case taxes on the cash at close, then imagine living on the remainder for five years under a non-compete (usually about three years, up to five).

-

The real target is a retirement number, not an exit. Take your annual need and divide by 5.5% (0.055). Example given: $200K per year divided by 0.055 is about $3.64M. The agency income should reach this independent of any exit; an exit just gets you there faster.

-

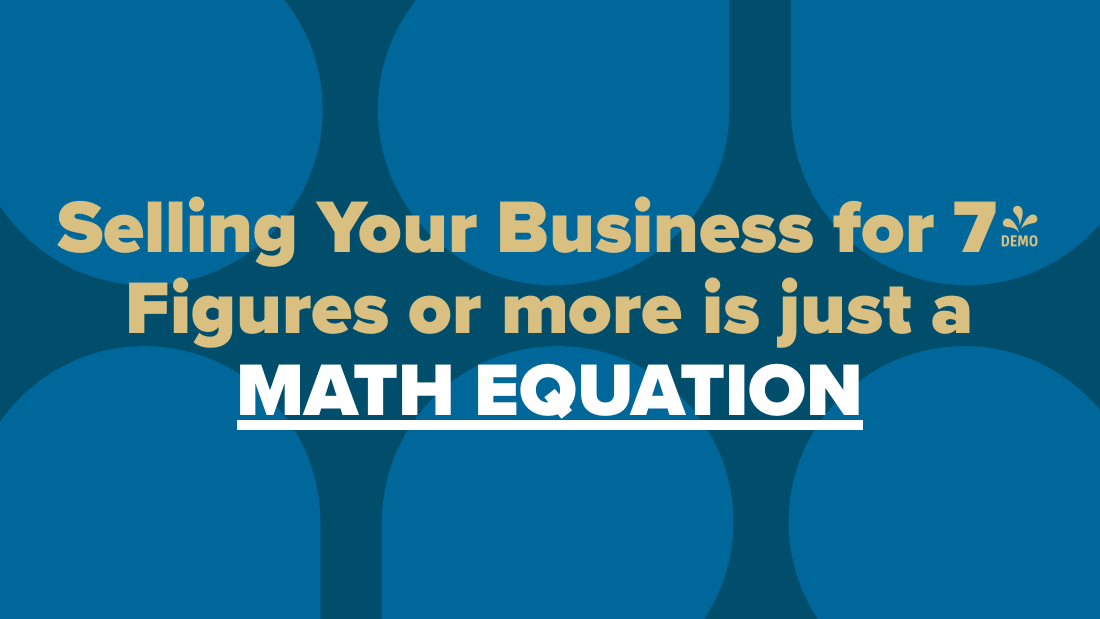

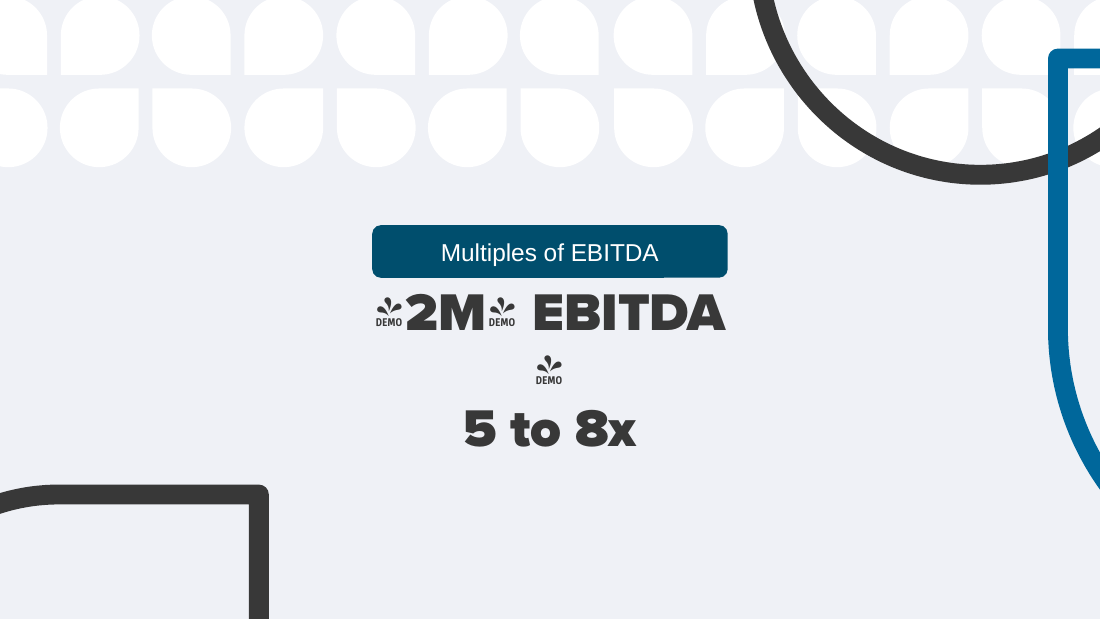

Selling for seven figures or more is a math equation built on EBITDA, not revenue. A sophisticated buyer cares mainly about EBITDA. Multiples scale with EBITDA size: under $1M EBITDA earns 2 to 4x, $1M to $2M earns 3 to 5x, and $2M+ earns 5 to 8x.

-

You need clean financials, an operator-led team, and healthy acquisition and retention to be sellable. The three must-dos are (1) Financials, (2) Team, and (3) Customer acquisition and retention. Missing the benchmarks inside each costs you "a turn" on the multiple (a 3x becomes a 2x).

-

Sellers who are not financially ready get squeezed. Those who are unprepared either shut their doors and walk away with nothing or take a bad self-financed (seller-financed) deal from "vultures," and may have to take a damaged business back.

Key points

The "real number" math

- Step 1: Write down the price at which you become a seller of your agency (the enterprise value).

- Step 2: Cut it in half. You typically get half in cash at close and half in an earn-out; if the buyers miss targets you may never get the second half.

- Step 3: Reduce by about 40% (worst-case taxes on the cash at close). On taxes specifically, Martinez deferred to a separate, tax-focused talk by another speaker (a different "Kyle") scheduled the next day.

- Step 4: Imagine living on the remainder for five years under a non-compete (usually about three years, can be up to five). Ask: is that enough?

Retirement number

- Retirement number = one year of income divided by 5.5% (0.055).

- Example: $200K per year divided by 0.055 is about $3.64M.

- Build the agency to reach this from income, independent of any exit; treat the exit as the accelerant ("the cherry on top").

The sell-side process (in order)

- Gather financials (minimum 3 years, most likely 4).

- Produce an estimate of business value (often before signing with a representative).

- Build a "data room" (described as a secure, expensive "fancy Google Drive").

- Select an attorney.

- Engage your CPA and start a tax plan (ideally at least a year before exit).

- Create an anonymous 1 to 2-page teaser PDF of business highlights and shop it to the buyer network.

- Have interested buyers sign an NDA.

- Send the CIM (Confidential Information Memorandum), a data-heavy PowerPoint sent after the NDA.

- Hold management meeting(s) (often Zoom; your team preps you "like preparing a witness").

- Collect IOI(s) (Indication of Interest): a value range and rough structure. Aim for multiple.

- Sign one exclusive LOI (Letter of Intent): the deal structure and earn-out details; usually a 90-day exclusive window with one buyer.

- Survive about 3 months of due diligence while still running the business and hitting your forecast. Missing a forecast in that window drops the price ("can't trust your 3-year forecast if I can't trust your 60-day").

- The agency M&A buyer network is small (described as "like forty people"); reputable reps shop teasers privately rather than listing on a website. (A Bloom partner named Reuben "has lunch with these people.")

- You want multiple buyers up to, but not through, the exclusive LOI; you can use late-comers against the field.

- Advice: if a representative is not following this process, run away.

Must-do 1: Financials (EBITDA multiples)

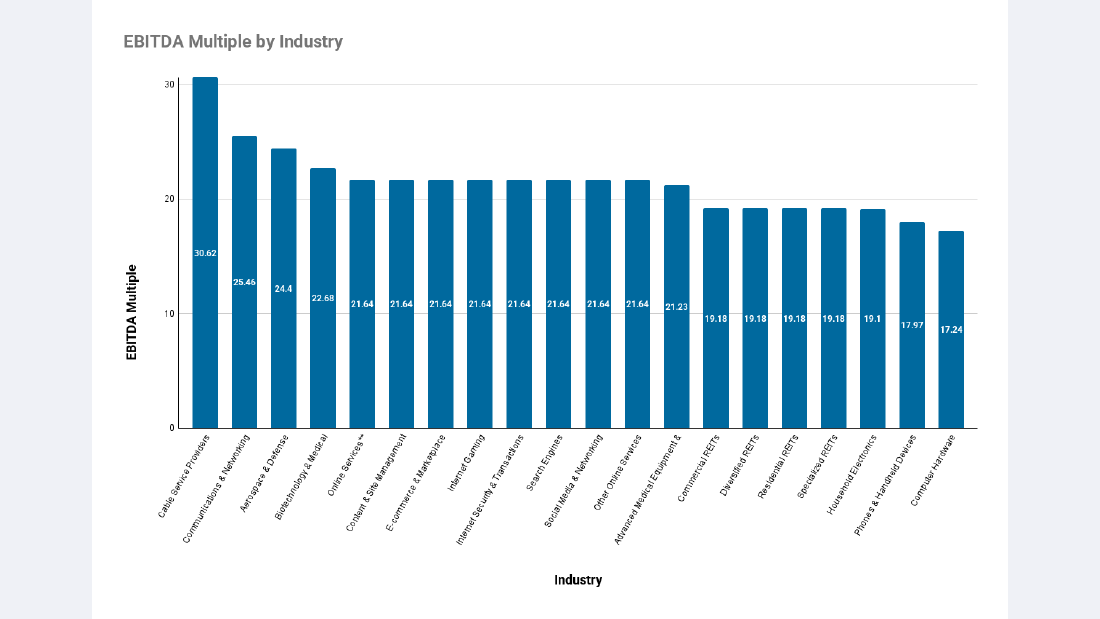

- A sophisticated buyer cares mainly about EBITDA, not revenue. EBITDA = earnings before interest, taxes, depreciation, and amortization; informally, the money the business makes after all expenses including your own salary, but before loans, taxes, and equipment costs.

- Under $1M EBITDA: 2 to 4x (most likely 3; e.g. $500K EBITDA is about $1M to $1.5M, rarely 2x).

- $1M to $2M EBITDA: 3 to 5x (e.g. $1.5M EBITDA is about $4.5M to $7.5M).

- $2M+ EBITDA: 5 to 8x ("I know somebody that got 12" was cited as an exception).

- Need at least 3 years of financials (many buyers ask for 4).

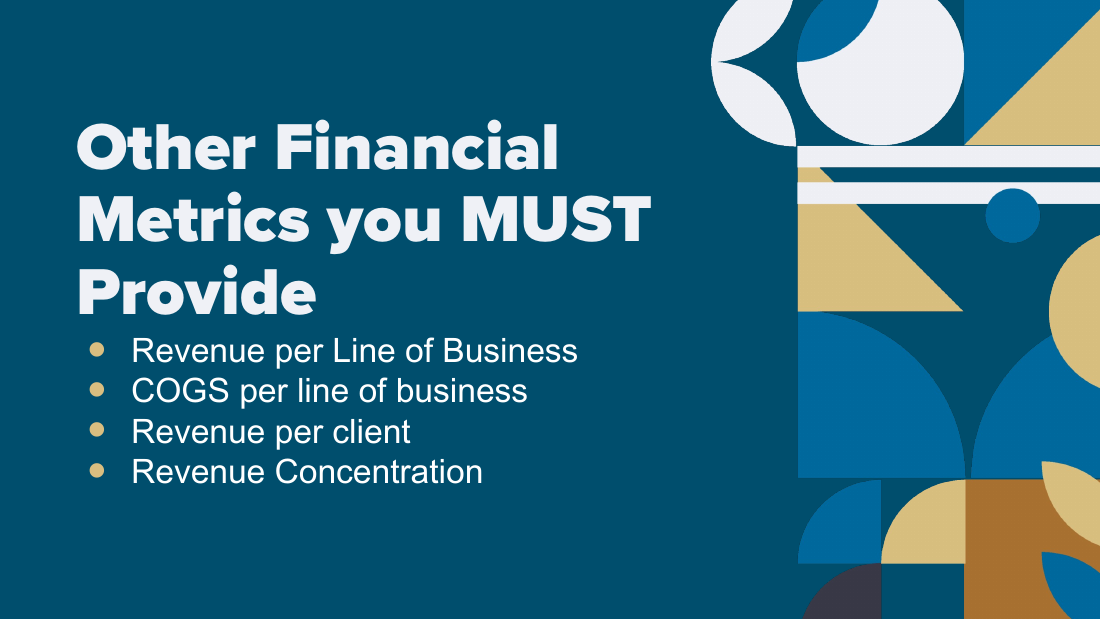

- Also required: revenue per line of business, COGS per line of business (he pushes time tracking; used a Chuck E. Cheese pizza-costing analogy), revenue per client, and revenue concentration.

- Revenue concentration: no single client should exceed 20% of total revenue, or you lose "a turn."

- Growth: about 20% year over year is ideal; under 10% loses a turn.

- Recurring revenue: about 80% monthly recurring or better; project work is very hard to sell.

- CAGR (compounding annual growth rate) is more a buyer-side / third-party verification metric, not something the seller splits out. (Martinez deferred a CAGR-vs-seller question.)

Must-do 2: Team

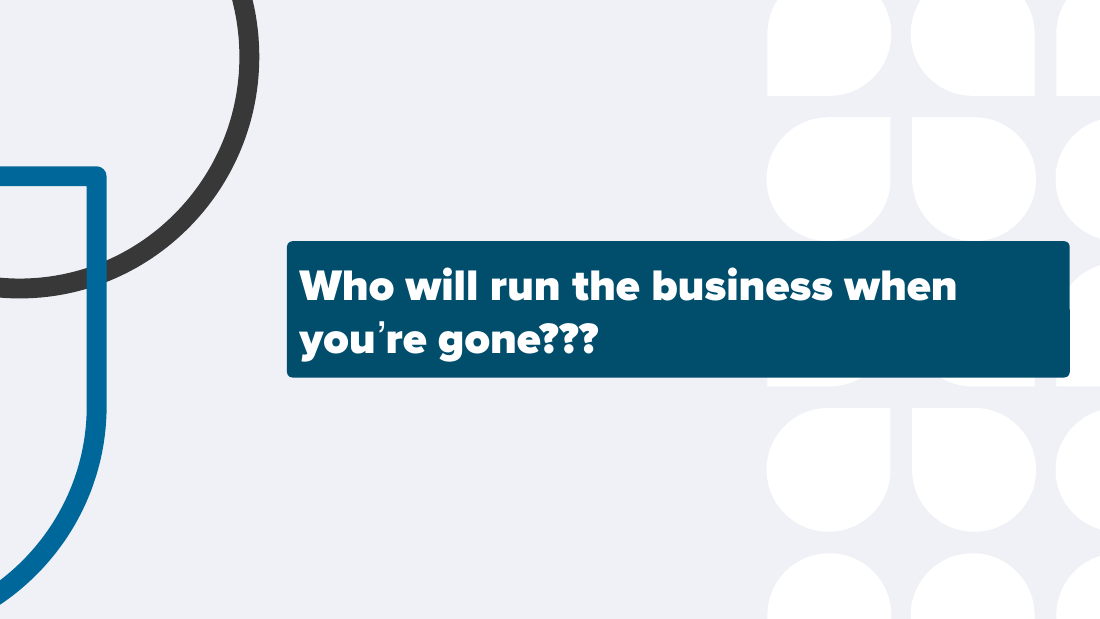

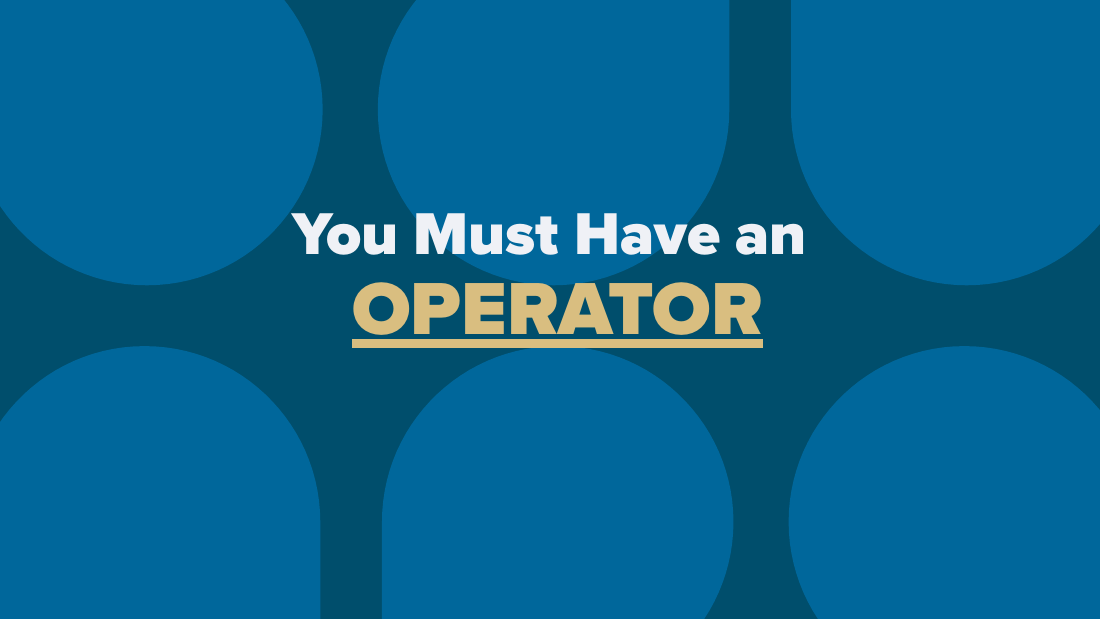

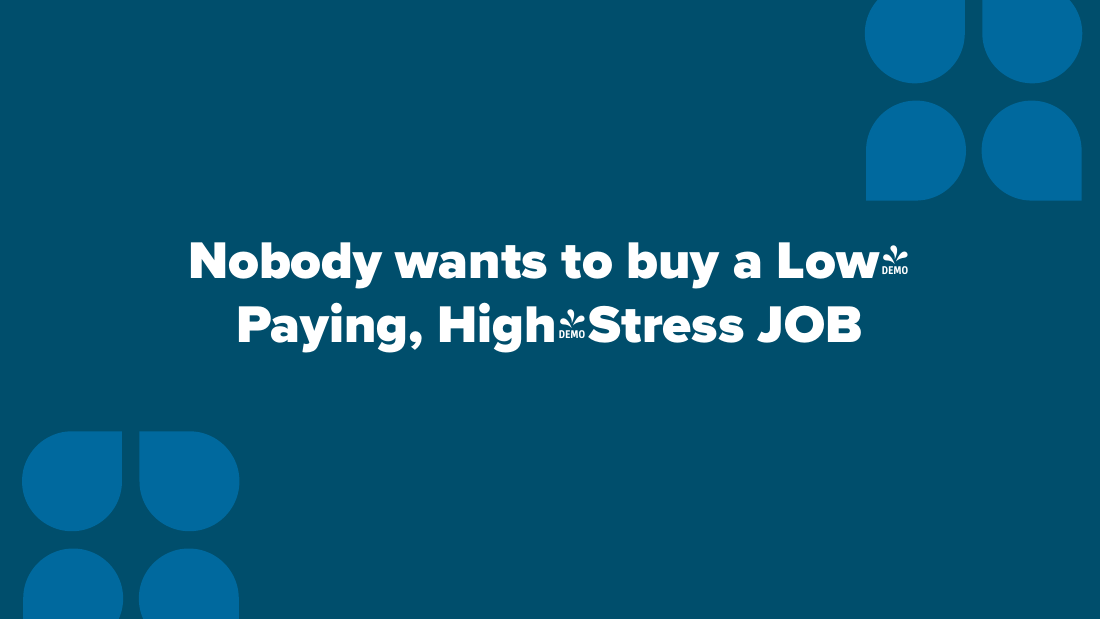

- "Nobody wants to buy a job" (a low-paying, high-stress one). You must have an operator (your number two) to run the business after you leave.

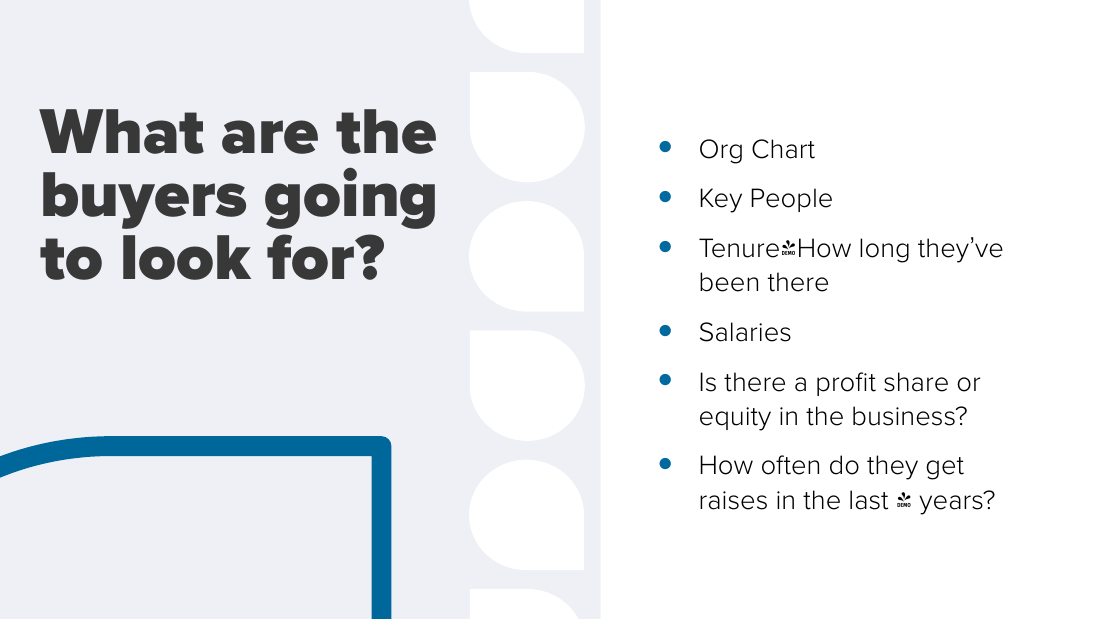

- Buyers look at: org chart, key people, tenure, salaries, profit share or equity, and raise/training history over roughly the last 4 years; they often interview the team.

- You do tell your key people they will go with the business. De-risk by financially incentivizing: a "kiss goodbye" bonus check, plus tying the earn-out to them staying (another check).

- The leadership team must be US-based, full-time, and W2. Production labor (freelancers/VAs) is more flexible: if the buyer already has a team and your people are contractors, they are easy to release, which can be a benefit.

Must-do 3: Customer acquisition and retention

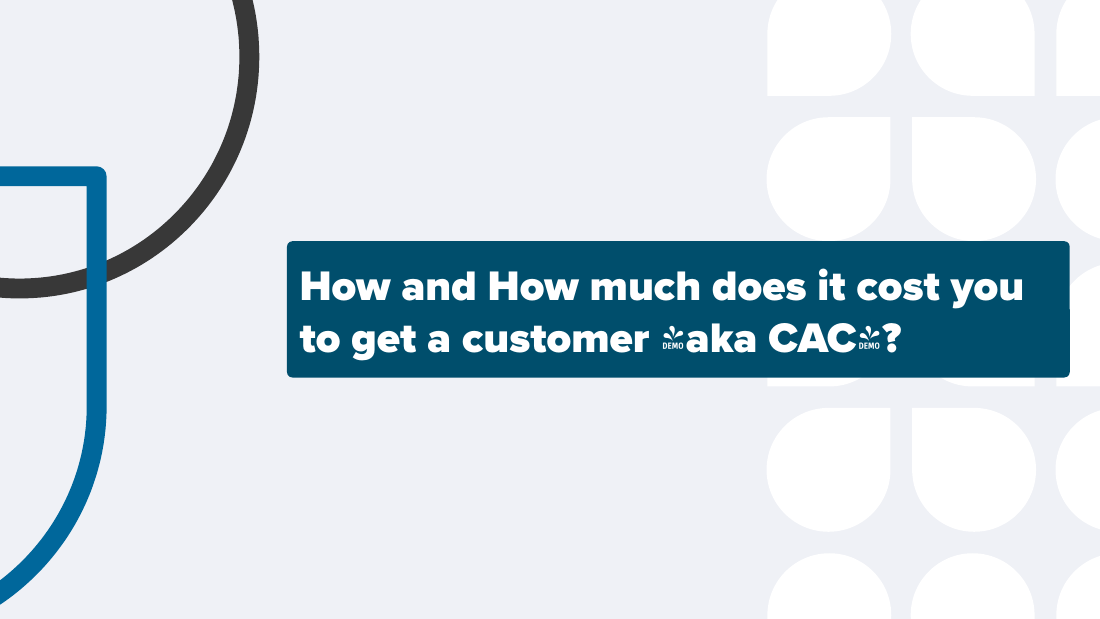

- Know your CAC (cost to acquire a customer). All-referral acquisition is harder to value, so have a strategy or an answer.

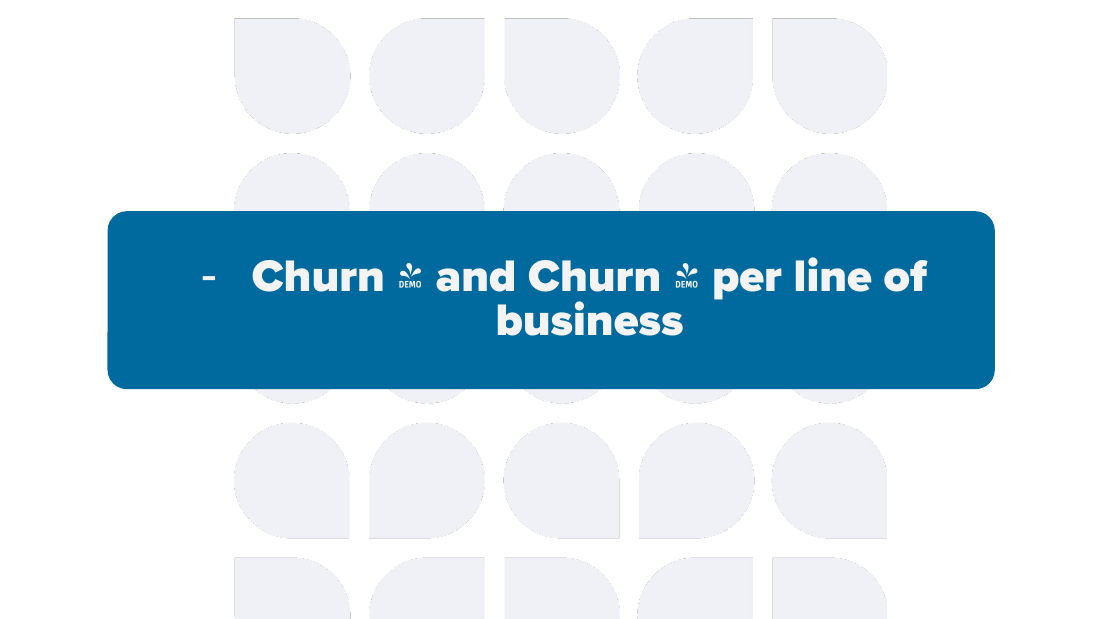

- Churn: percentage of clients lost per month; track it per line of business (churn differs by what was bought). Martinez said it has "never been worse."

- LTV formula: take 1 divided by your monthly churn rate as a decimal to get the number of months a client stays, then multiply by average revenue per month. Example: 3% monthly churn means 1 / 0.03 is about 33.33 months, multiplied by average monthly spend. (3% is described as "what it should be per month.")

Other Martinez points

- "Revenue is vanity, profit is sanity... all that matters is what you keep."

- Mid-market squeeze: very low-ticket and high-ticket agencies did okay over the past roughly 18 to 24 months; agencies charging about $1,000 to $3,000 per month "are getting squeezed."

- Sellers who are not financially ready end up either shutting their doors for nothing or taking a bad self-financed deal from "vultures" (and may have to take a damaged business back).

- A directory website (not named) spun off a low-ticket agency and a low-ticket SaaS (about $25/mo) and struggled to find a single buyer for all three; low ticket means no upsell room. Advice: "keep it simple."

- AI can now evaluate businesses "in minutes instead of weeks."

- Bloom Partners: management consulting (HR and finance for agencies) plus agency M&A. The team has done $700M+ in total M&A and $200M+ in agency M&A (spoken figure; the deck speaker-notes say $250M).

- Martinez is now President (moving to CEO) of BPO Solutions Group (overseas staffing for the Fortune 1000), targeting a $100M valuation in 3 years.

- Credentials: 2-time Stevie Award winner, 4-time author (last book "Facts Not Feelings"). Contact given on stage: Chris@BloomPartners.io. A free "exit checklist" PDF was offered. (This was a pitch-free session per the event code of conduct.)

Slides

Slides (49)

Source

Synthesized from Chris Martinez's SEO Spring Training 2026 session (Day 1), drawn from the conference transcript and his deck "Martinez FINAL 3 Must-Dos to Prepare Your Agency for Sale SEO Spring Training 2026.pptx." This page covers only Martinez's portion of a three-speaker block. The deck team-M&A figure differs between the spoken talk ($200M+ agency M&A) and the deck speaker-notes ($250M+). Several specifics were not named on stage: the tax-talk speaker (a different "Kyle"), the unnamed directory website, and the free exit-checklist download URL.